Travel Remains a High Priority for Americans as Financial Sentiment Shows Signs of Stabilizing

As Americans move through the first quarter of 2026, travel continues to hold its place as one of the most resilient household priorities. Financial sentiment among American travelers appears to be stabilizing, and while optimism about the year ahead remains somewhat cautious, Americans continue to invest in travel—evidenced by rising travel budgets and strong early indications for the upcoming summer season.

Current financial sentiment remained steady month-over-month, with 33.9 percent of American travelers reporting that their household is financially better off compared to a year ago (vs. 33.4% in January 2026). This represents a modest +1.2 percentage point increase compared to the same point in 2025. At the same time, the share of travelers who feel financially worse off has declined to 20.8 percent this month (-2.7pp versus January 2026 and -2.3pp versus February 2025), suggesting that financial pressures may be easing slightly for some households.

While current financial conditions show signs of stabilization, expectations for the year ahead remain somewhat more cautious. The share of American travelers who expect to be better off financially in the next 12 months rose modestly to 45.5 percent (+0.6pp month-over-month), though it continues to track slightly below the same time last year (-0.7pp).

Recession expectations among travelers have also continued to decline. The share expecting a U.S. recession in the near term fell for the fourth consecutive month to 40.4 percent (-1.6pp month-over-month and -1.5pp year-over-year). Taken together, these indicators suggest that the economic outlook among American travelers was relatively stable at the time the survey was conducted. It should be noted that this month’s survey was fielded between February 17 and March 3 and therefore includes responses collected following the start of recent U.S. military operations in Iran.

Looking at how these financial signals are translating into travel spending behavior, 35.7 percent of American travelers say now is a good time to spend on travel, up slightly from last month (+0.9pp), though marginally lower than the same time last year (-1.0pp).

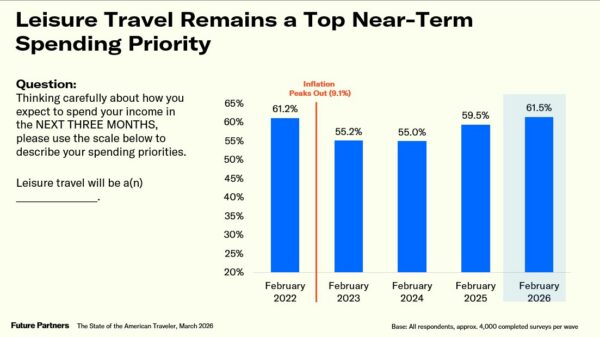

More notably, travel continues to rank highly among near-term household priorities. Over six in ten American travelers (61.5%) say travel is a high spending priority for the next three months, up +3.0 percentage points compared to January 2026 and +2.0 points higher than a year prior.

Perhaps the clearest signal of Americans’ continued commitment to travel this year is the steady rise in anticipated travel budgets. The average maximum annual leisure travel budget reached a new record high of $6,556, surpassing January’s previous peak and reinforcing the willingness of many households to allocate meaningful resources toward travel in the coming year.

Recent Trip Volume and What’s Ahead

With travel remaining a high priority for many households, Americans are continuing to translate intent into real travel activity. Following the winter holiday travel season, current travel volume shows a mixed but generally healthy pattern across trip types.

Less than half of American travelers (47.5%) reported taking an overnight leisure trip in the past month, down slightly from the month prior (49.7%) but still higher than the 43.2 percent reported at the same time last year. Overnight trips to visit friends and relatives were taken by 42.3 percent of travelers last month, representing an -8.0 percentage point decline month-over-month but remaining essentially flat compared to February 2025 (+0.2pp).

Day trips, however, remained comparatively strong. Just over half of American travelers (50.8%) reported taking a leisure day trip in the past month, up from both January 2026 (49.6%) and February 2025 (48.5%). Meanwhile, 40.9 percent reported taking a day trip to visit friends and relatives, though this metric declined slightly both month-over-month (-5.2pp) and year-over-year (-3.3pp).

These results suggest that while the typical post-holiday slowdown is visible in overnight travel, overall travel activity remains healthy as Americans begin planning for the peak spring and summer travel seasons.

Among demographic groups, Millennials were more likely than other generations to report taking any overnight or day trip in the past month. Parents of school-aged children also over-indexed across all trip types, including overnight leisure trips (58.0%), overnight trips to visit friends and relatives (48.3%), leisure day trips (60.1%), and day trips to visit friends and relatives (49.0%).

Looking ahead, American travelers expect to take an average of 4.1 leisure trips over the next 12 months, slightly above both last month (4.0 trips) and the same time last year (4.0 trips). Income remains the strongest differentiator in anticipated travel activity. Travelers in households earning $200K or more expect to take the most trips on average (5.2), followed by those earning $100K–$199K (4.5 trips). Travelers earning $50K–$99K anticipate taking 3.8 trips on average, while those earning less than $50K expect approximately 3.3 trips in the coming year.

Summer Travel Outlook

As the travel industry begins turning its attention toward the upcoming summer season, American travelers are already showing strong travel intentions.

On average, travelers report planning 1.7 overnight leisure trips between Memorial Day and Labor Day, with 78.8 percent saying they currently have at least one trip planned. Among those with summer travel plans, nearly half (46.7%) have already fully booked at least one overnight summer trip, indicating a strong level of commitment to travel in the months ahead.

Most of these trips are expected to take place within the United States, with 67.0 percent of currently planned summer travel destined for domestic locations.

When asked about their primary motivations for traveling this summer, relaxation tops the list (58.0%), followed by visiting friends and relatives (47.9%) and escaping everyday stress (40.6%). These motivations highlight travelers’ continued desire for restorative and socially meaningful experiences.

American travelers are also prioritizing experiences that emphasize outdoor settings and local culture. Beaches lead the list of desired summer experiences (41.0%), followed by exploring the local food scene (27.2%), scenic drives (27.1%), and visits to state or national parks (26.8%).

At the same time, travelers remain mindful of potential challenges when selecting destinations. Excessive heat ranks as the leading concern (40.1%), followed by crowds (36.7%) and political unrest or protests (32.6%). Environmental risks also factor into destination decisions, with roughly one in four travelers citing wildfires (26.7%) or hurricanes (22.8%) as concerns for their summer travel plans. These findings reinforce that while summer travel demand remains strong, safety and climate-related considerations are increasingly shaping destination choices.

FIFA World Cup Outlook

In addition to summer travel planning, the United States is rapidly approaching the 2026 FIFA World Cup. This month’s survey revisits American travelers’ interest in traveling specifically to attend World Cup events.

Overall, interest in traveling for the event remains moderate among American travelers, with 23.6 percent expressing some level of interest. However, enthusiasm rises significantly among several key demographic groups, highlighting important opportunity audiences for host destinations. Millennials show the highest level of interest (41.2%), followed by parents of school-aged children (37.7%) and Hispanic/Latino travelers (35.7%). Urban residents also display elevated enthusiasm for World Cup travel (35.1%).

Conversely, interest is notably lower among Baby Boomers (11.9%), rural residents (10.8%), and travelers based in the Midwest (18.2%).

Among travelers who say they are interested in attending a World Cup event, most anticipate making an overnight trip tied to match attendance. About 44.5 percent say they would stay overnight to attend a single match, while 30.5 percent would stay overnight to attend multiple matches. A smaller share (17.0%) say they would plan a day trip for a single match, while only 2.3 percent say they would attend official fan festivals or other fan events without attending a match. About 5.7 percent remain undecided about how they would structure their trip.

When considering potential host destinations, Los Angeles (33.0%), Miami (30.1%), and New York City (29.8%) emerge as the most appealing locations. As expected, proximity and regional accessibility continue to play an important role in shaping destination preferences for potential World Cup travelers.

Looking Ahead

Taken together, these latest findings suggest that American travelers are entering the spring and summer travel seasons with growing financial stability and sustained enthusiasm for travel. While economic uncertainty remains part of the broader backdrop, Americans continue to prioritize meaningful travel experiences—supported by rising travel budgets, steady travel activity, and strong early summer travel plans.

For the complete set of findings, including data on your audience segments and historic brand performance of your travel brand or destination, subscribe to The State of the American Traveler Insights Explorer tool.

Learn more about the latest trends during our monthly livestream.

To make sure you receive notifications of our latest findings, you can sign up here.

Have a travel-related question idea or topic you would like to suggest we study? Let us know!

We can help you with the insights your tourism strategy needs, from audience analysis to brand health to economic impact. Please check out our full set of market research and consulting services here.